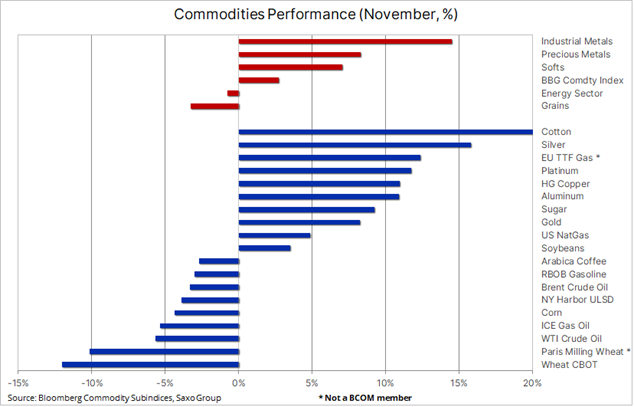

The Bloomberg Commodity Index Total Return index traded up 2.7% in November, thereby driving the index to a 19% gain on the year. The strong gains among industrial and precious metals offset the minor decline in energy and grains prices. Following several challenging months, the metal sectors found support from a weaker dollar and sharply lower bond yields, both driven by a lower-than-expected US CPI print last month. The emerging weakness in US economic data has led to speculation that the US Federal Reserve may soon slow its pace of rate hikes.

A development that was confirmed by Fed Chair Powell in a speech on Wednesday when he signaled a smaller December rate hike as he presented a case for achieving lower inflation without tipping the economy into a deep recession. Whether successful or not may turn out to be a major driver of risk sentiment into 2023, with precious metals especially standing to benefit should he fail.

The industrial metal sector jumped 14.5% on the month, thereby reducing the year-to-date loss to 4.5%. The primary driver, apart from the softer dollar, is the optimism that China may shift away from Covid Zero policies and provide additional stimulus to boost demand in the top metal-consuming economy. Copper jumped 11% last month to record its best month since April 2021 and its first monthly advance since March. Having started the year on a high note driven by post-Covid optimism, the subsequent and prolonged Covid zero focus in China drove the price sharply lower from March onwards. The result of this is a metal that, despite the strong November, remains down 17% on the year.

The precious metal sector also recorded a strong month of November as the Bloomberg Precious metal index rose by 8%, thereby reducing the annual loss to just 5%. Silver led the charge with a 16% gain to $22.16, clawing back half of the losses that was seen between the March peak at $30 and the September low at $17.50. Gold, out of favor for months by traders and investors as the dollar and Treasury yields surged higher, managed a strong turnaround, rising 8% to reach $1768 – thereby reducing the year-to-date loss in dollar terms to just 3.3%. This is impressive in a year that, despite the recent weakness, has seen the dollar surge by 8% while US ten-year real yields have surged higher by around 2.3%.

Silver’s impressive rally has continued into December with the price breaking above $22.25 – a 50% retracement of the March to September selloff – and on route to the next level of resistance at $23.35. Meanwhile, gold is currently working its way through a key area of resistance between $1788 and $1808. However, with the market increasingly focusing on a Fed pivot, potentially without getting inflation under control, an upside break would confirm a cycle low around $1615 and with that a potential push higher.

Crude oil recovers from unwarranted China demand scare

The energy sector suffered a small setback in November but remains up 55% on the year due to very strong gains in diesel and gasoline as well as natural gas. In November, all the major contracts, with the exception of natural gas, traded lower as the market took fright from continued lockdowns in China, a seasonal slowdown in demand and a steeply inverted US yield curve increasingly pointing in the direction of a sharp economic slowdown next year.

Crude oil spent the week recovering from a ten-month low after renewed and, in our opinion, unfounded worries about a deteriorating demand outlook in China. The bounce was supported by a weaker dollar and traders assessing signals that China may soften its Covid Zero policy after China’s Vice Premier in charge of fighting Covid acknowledged the Omicron variant is less deadly.

These developments forced a reduction in recently established short positions ahead of Sunday’s OPEC+ meeting. A meeting that is likely to be strong on words but low on actions, considering the unclear impact of an EU embargo on Russian oil starting on 5 December. In addition, US crude stocks fell by 12.6 million barrels last week, the biggest decline since June 2019, while US crude and product export hit a record close to 12 million barrels per day – highlighting continued strong demand from buyers looking for alternative supplier than Russia. In addition, the US government is likely to halt sales of crude from its Strategic Reserves soon, thereby removing an important source of supply which has seen 205 million barrels flow into the market this year.

Recession versus tight supply

The risk of an economic downturn at a time of tight supply of several major commodities will be one of the key battlegrounds that, together with the strength of a post-Covid recovery in China, will help determine the direction of commodities in 2023. Following months of aggressive rate hikes, the US Federal Reserve is now signalling a slowing pace of future rate hikes – with the eventual peak rate being determined by incoming data. From an investment perspective, the commodity sector has beaten most other asset classes this year and, despite a recent softness and easing of tightness, we maintain the view that investors should maintain a broad exposure to commodities into 2023.

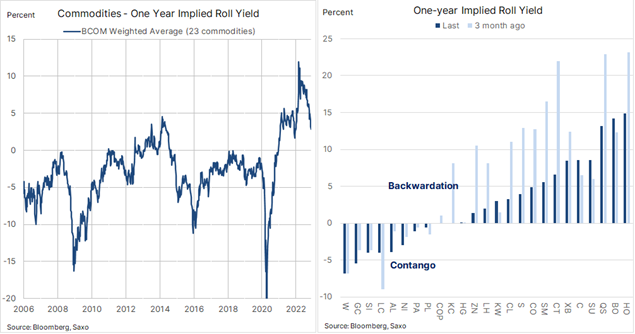

The one-year implied roll yield, using a weighted average of the 23 commodities in the Bloomberg Commodity Index, remains positive, albeit lower than at the start of the year. The positive roll yield or backwardation signals a tight market outlook across most commodities currently led by commodities from energy, grains and softs.

A positive roll yield, i.e. selling an expiring futures contract, at a higher price than where the next is bought, has supported the strong return investors have achieved through an investments via futures and ETFs this year. The chart below shows the year-to-date performance of an ETF tracking the Bloomberg Commodity Total Return Index and the Bloomberg Spot index which excludes the extra income achieved from the roll yield. Year to date, the ETF has realised a 17.6% return while the underlying spot index has delivered a six percent lower return. We expect the tailwind from tight markets trading in backwardation will rise again over the coming months. Not least driven by increased tightness across the energy complex as the embargo on Russian oil and, from next year, fuel products increasingly adds upward pressure on the front end of the forward curve.